# Research Summary

source: https://developer.mastercard.com/unified-installments/documentation/experience-design-guide/pre-approved-offers-in-lender-app/research-summary/index.md

### What we learned was invaluable {#what-we-learned-was-invaluable}

To make the experience true to the mission, we asked hundreds of consumers, to test the Mastercard Installments solution and provide feedback. Using the insights from the research, we updated the flows and tested again. We completed this process multiple times throughout the design process. To learn more, we provide a consolidated summary below that includes the criteria and results from the different rounds of testing.

### Round 1 {#round-1}

Mix of moderated and unmoderated tests with participants from UK, MEA and Australia (credit card/non-credit users) in age group of 18 - 54 years

##### What we tested {#what-we-tested}

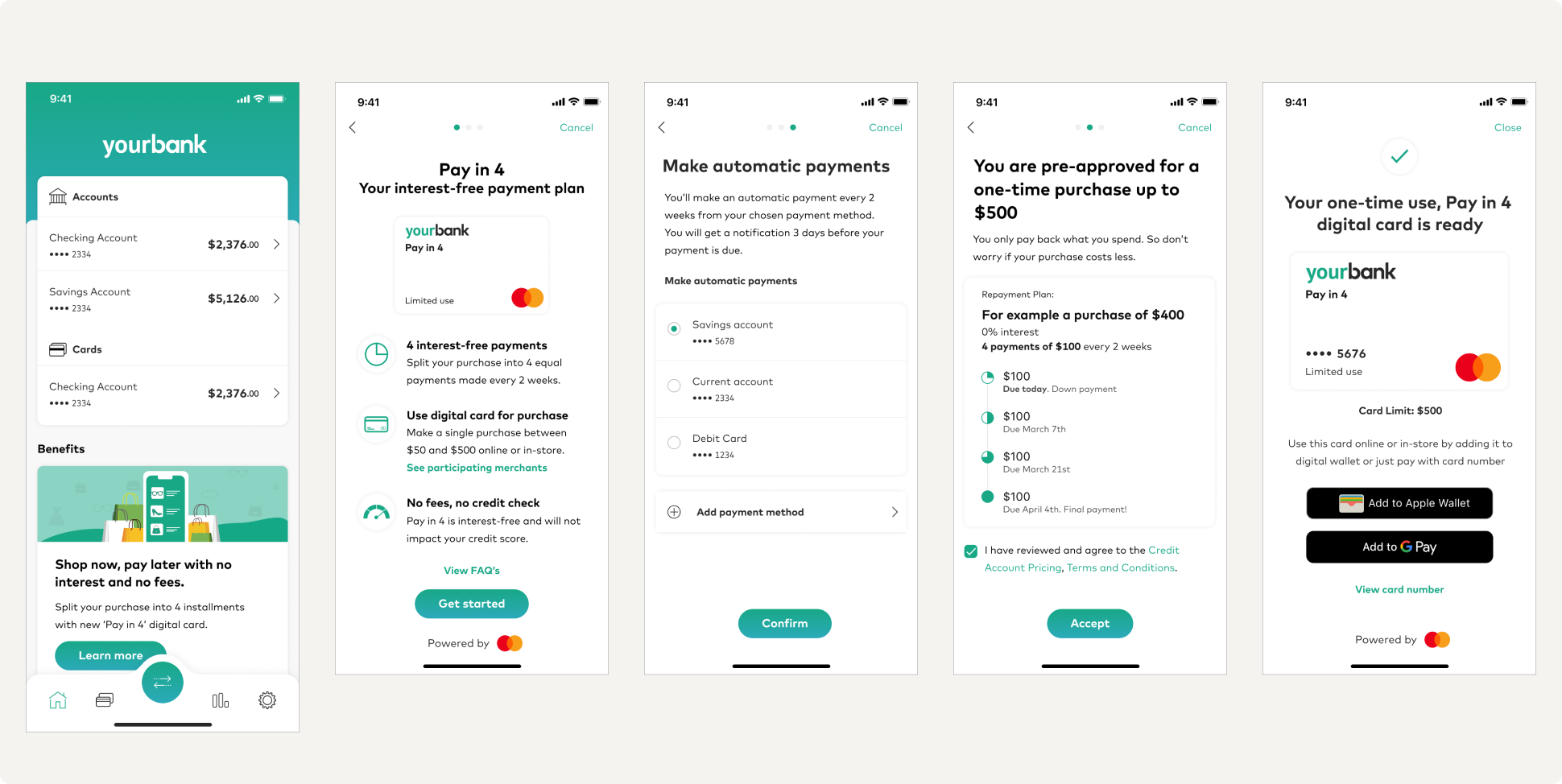

* Card issuance UX

##### What we learned {#what-we-learned}

* A familiar yet novel concept, participants across regions saw the value of being able to split a large purchase, or several large purchases, equally over the course of few months (3,4 or 6).

* Notion of 'No fees and no interests' attracted all users across regions.

* Users saw the offer could be useful when making larger or more substantial purchases, as a means of budgeting.

* 81% of visitors in UK who hoped for interest-free payments were satisfied with the offering; they liked the notion of paying the same amount of money they used for their purchase.

* 72% in Australia said they would stick to a 6-month term, whereas 28% say they would like the option to extend, especially during uncertain times.

* Potential users appreciated that the language used throughout the experience was simple and jargon-free, allowing them to have a good overall understanding of the offering.

* However, respondents in all regions found the phrases "limited use," and "pre-approval" to be confusing and somewhat misleading.

* 'Digital Card' was the term preferred over 'Virtual card' across user groups in every region. (73% users in UK, 53.06% in MEA and 76% in Australia)

* Overall users wanted to make multiple purchases with the digital card. In the UK, 60% of visitors indicated it was more convenient and allowed them to keep track of their spending while in Australia, 72% preferred option for multiple purchases as it allowed more versatility.

* However, in the UK, it was also observed that there were users seeking 'One-time use' card to make an occasional, intentional purchase as it fitted the model of a short term loan. One-time use also appealed the users who wanted to be more disciplined with their finances and preferred to not run multiple payment plans.

* Data security was found as a top priority, and of those who express security-related concerns, nearly 65% wanted to know more about data privacy and security protocols.

* In addition, there was a persisting curiosity amongst respondents regarding how much control they will have over their payment schedule and wanted more clarity around the late fees.

#### Outcomes from Round 1 {#outcomes-from-round-1}

* As a result of our research, we updated the flows with improved content, addressed user queries through better FAQs, included multiple options to help users understand where they can use their digital cards.

### Round 2 {#round-2}

Unmoderated tests with participants from UK \& USA (credit card/non-credit users who were familiar with BNPL concept) in age group of 18 - 54 years

##### What we tested {#what-we-tested-1}

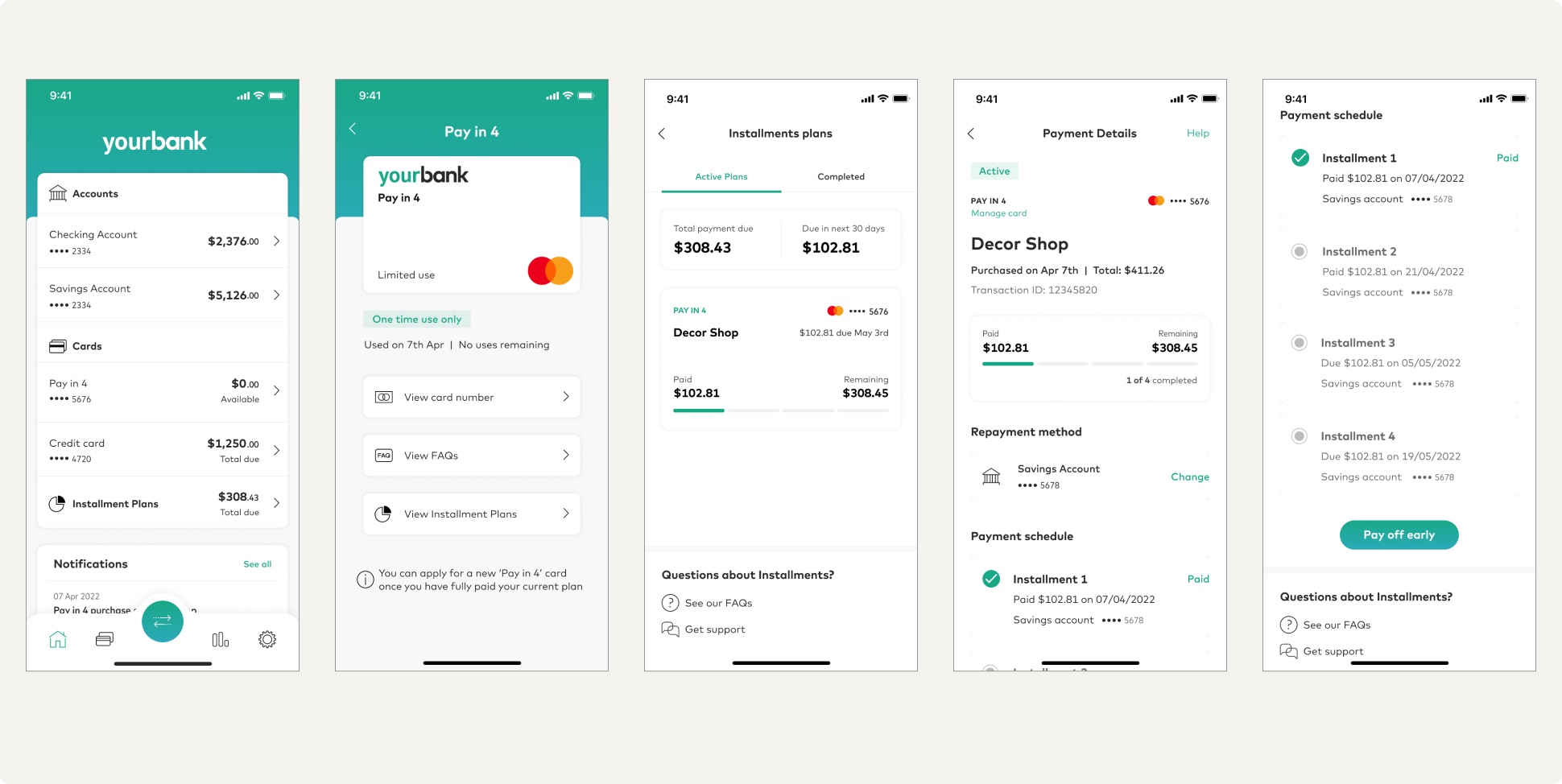

* Post purchase UX

##### What we learned {#what-we-learned-1}

* Potential users found the experience to be well-organized and intuitive, providing them with clear steps and information regarding making relevant payments.

* Users showed good amount of trust in the product as it came from their bank and Mastercard.

* Respondents voiced positive sentiments over the colours, resources, visuals, and relevant information throughout the journey.

* The breakdown of the payment schedule was easy to understand and provided users with a clear picture of their paid and outstanding debts in both the regions.

* Users appreciated the tabular design as it helped them quickly find details of their card and the plan

* While many users voice positive sentiments towards the immediate highlighting of their total amount due on landing screen, for some users, inclusion of duplicate information, such as amounts owed on each page, felt unnecessary.

* Given a choice to pay off early, in UK, 53% said they would pay full remaining amount, 34% would pay as per the schedule, and 13% chose pay next installment while in the US, 47% said they would pay full remaining amount, 27.8% would pay as per the schedule, and 25.2% chose pay next installment.

* Regarding replenishment options for the multi-use card option tested in the UK, 54% selected "Amount added back after every instalment is paid," 39% said "Amount added back after full payment of the instalment plan," and only 8% chose "Amount not credited back to the balance but an option to apply for a new card will appear when no balance is available to spend."

* In the US, where one-time use card was tested, it was observed that more clarity around how 'one-time use' card functioned was needed as some users were confused with how it works.

* 77.5% users in US also said they would consider to reapply only after paying off the on-going plan while 22.5% users were open to apply for new digital card alongside an already running active plan.

* Overall in the UK, for 91% users, overall experience was clear without the need of further support and only 9% felt some parts of the experience was confusing and in the US, 97% indicated that the experience somewhat met their expectations of which 62% mentioned their expectations were fully met.

#### Outcomes from Round 2 {#outcomes-from-round-2}

* As a result of our research, experience was updated with improved content and some changes in the design considering the scalability factor when the app would also include the digital cards issued at the merchant site in later stages of development.

Next: [Prepare for launch](https://developer.mastercard.com/unified-installments/documentation/experience-design-guide/pre-approved-offers-in-lender-app/prepare-to-launch/index.md)